An invoice is a request for payment a seller sends before money changes hands. A bill is that same document seen from the buyer's side — an amount they owe. A receipt is the proof issued after payment confirming money was received. In short: invoice = "please pay," bill = "I owe," receipt = "paid in full." In India, GST adds one more layer — a tax invoice versus a bill of supply.

Quick answer: invoice vs bill vs receipt

- Invoice — issued by the seller before payment; itemises goods/services and requests payment.

- Bill — the buyer's name for the same document; an amount payable.

- Receipt — issued after payment; confirms money was received and closes the transaction.

- Tax invoice — a GST invoice showing CGST/SGST or IGST so the buyer can claim input tax credit.

- Bill of supply — issued for GST-exempt goods or by a composition dealer; shows no GST.

What each document actually means (and why it matters)

| Document | Issued by | Issued when | Purpose | Why it matters |

|---|---|---|---|---|

| Invoice | Seller | Before payment | Requests payment, itemises supply | Creates a legal record of what is owed; basis for GSTR-1 |

| Bill | Buyer's view of the invoice | On receipt | States the amount payable | Used for accounts payable and expense tracking |

| Receipt | Seller | After payment | Confirms payment received | Proof of payment; needed for reimbursement and HRA claims |

| Tax invoice | GST-registered seller | On supply | Shows GST split for ITC | Lets the buyer claim input tax credit; mandatory if registered |

| Bill of supply | Composition dealer / exempt supply | On supply | Records a non-taxable sale | Legal substitute for a tax invoice where no GST applies |

Plain-English rule: the same piece of paper is an invoice to the person sending it and a bill to the person paying it. Once it is paid and stamped "Paid," it becomes a receipt.

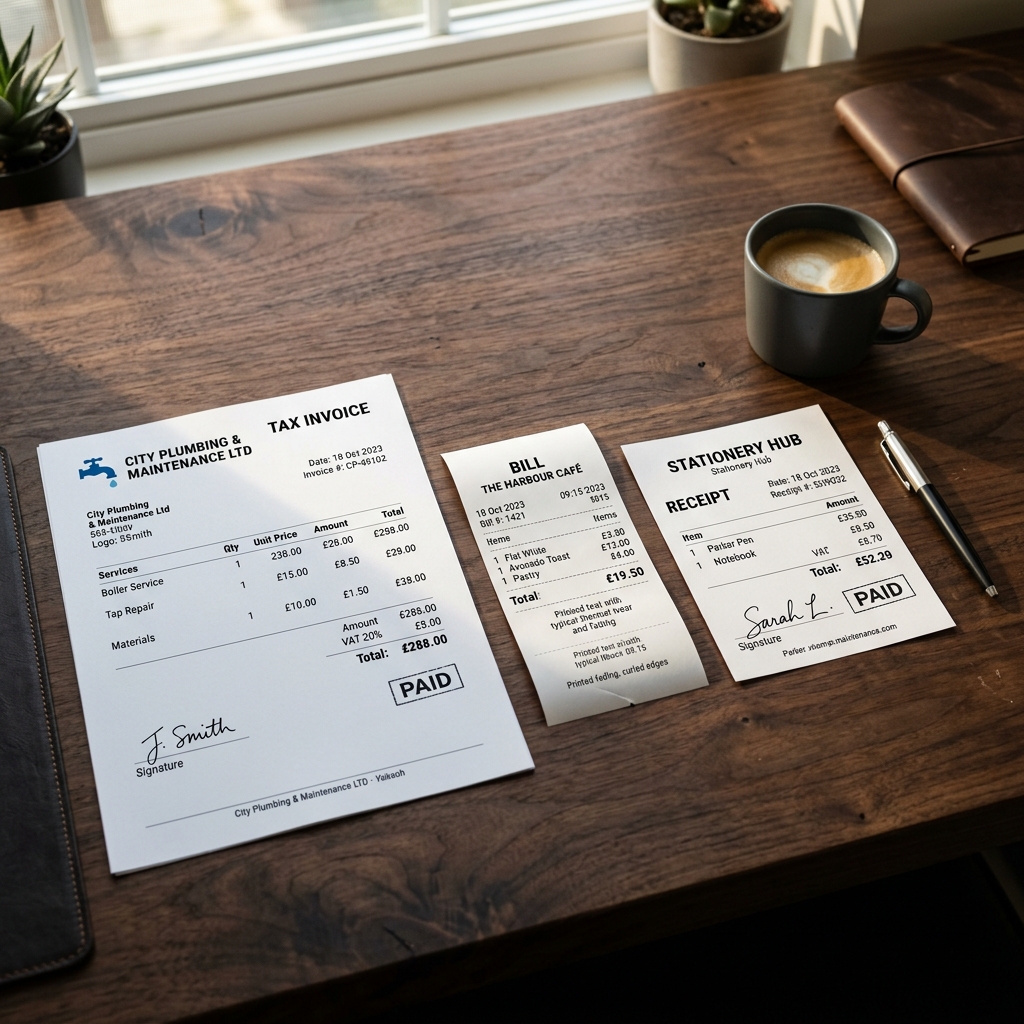

Annotated sample: one document, three stages

Here is a single transaction between an Ahmedabad wholesaler and a retailer, shown as it moves through all three stages with realistic dummy data.

Stage 1 — Invoice (seller requests payment):

Patel Distributors Pvt. Ltd. (prop. Mehul Patel) 14 Ashram Road, Ahmedabad, Gujarat 380009 · GSTIN: 24AAACA7788N1Z4 Tax Invoice: INV-2026-00471 · Date: 01 Jun 2026 Bill to: Trivedi General Store, Gandhinagar · GSTIN: 24AAGCV2201C1Z1

| Item | Qty | Rate (₹) | Amount (₹) |

|---|---|---|---|

| Aashirvaad Atta 10 kg | 20 | 480.00 | 9,600.00 |

| Tata Salt 1 kg | 50 | 28.00 | 1,400.00 |

| Subtotal | 11,000.00 | ||

| CGST @ 2.5% | 275.00 | ||

| SGST @ 2.5% | 275.00 | ||

| Grand Total | 11,550.00 |

Status: UNPAID · Due within 15 days

Stage 2 — Bill (buyer's books): Trivedi General Store records the same ₹11,550 under accounts payable as a bill owed to Patel Distributors.

Stage 3 — Receipt (seller confirms payment): Once Trivedi pays by NEFT, Patel issues:

Receipt No: RCPT-2026-00471 · Date: 14 Jun 2026 Received from Trivedi General Store the sum of ₹11,550.00 Against Invoice INV-2026-00471 · Mode: NEFT (UTR 552901xxxx) Status: PAID IN FULL

The GST layer: tax invoice vs bill of supply

This is the India-specific distinction that trips most people up. Under the CGST Act and rules(opens in new tab), the document you must issue depends on your registration status and what you sell:

- Tax invoice — issued by a regular GST-registered supplier. It must carry your 15-digit GSTIN, a unique sequential invoice number, the HSN/SAC code, and the CGST + SGST (same state) or IGST (inter-state) split. This is what lets your buyer claim input tax credit.

- Bill of supply — issued when you supply GST-exempt goods/services, or when you are registered under the composition scheme. It shows no tax amount and the buyer cannot claim ITC.

- Receipt voucher — under GST, if you take an advance payment, you issue a receipt voucher at that point, then the tax invoice when the supply is made.

Threshold note (FY 2025–26): GST registration is generally required once turnover crosses ₹40 lakh for goods or ₹20 lakh for services (₹20 lakh / ₹10 lakh in special-category states). Below this, you may operate unregistered and issue a plain bill without GST — see our guide on billing for an unregistered business. Always confirm current thresholds on the CBIC GST portal(opens in new tab).

For the full field-by-field breakdown of a compliant tax invoice, see what a GST bill must include, and for the maths of the tax split, see how to calculate GST on your bill.

A note on the proforma invoice. A proforma is not in this trio. It is a preliminary quote sent before the deal is confirmed — no GSTIN obligation, no entry in your books, no demand for payment. Read more in what is a proforma invoice.

Create an invoice, bill, or receipt in 2 minutes

You do not need accounting software to issue any of these. Using the bill & invoice generator:

- Pick the document type — invoice, bill, or receipt — from the template.

- Enter your details — business name, address, and GSTIN (saved for next time).

- Add line items with quantity and rate; the tool computes CGST + SGST automatically.

- Set the status — leave it "Unpaid" for an invoice, or mark "Paid" with a payment mode to turn it into a receipt.

- Download a clean PDF ready to print, email, or send on WhatsApp.

Online generator vs Word vs Excel/manual

| What matters for invoice/bill/receipt | Online generator | MS Word | Excel / manual |

|---|---|---|---|

| Flip the same doc from "Unpaid" invoice to "Paid" receipt | Yes Toggle status | No Rebuild by hand | No Rebuild by hand |

| Tax-invoice vs bill-of-supply layout (GST shown or hidden) | Yes Switches automatically | Partial Two saved templates | Partial Two saved templates |

| Unique, gap-free invoice numbering for GSTR-1 | Yes Counter never repeats | No Easy to duplicate | Partial Manual sequence |

| Linking a receipt back to its original invoice number | Yes Carried over | No Re-key by hand | No Re-key by hand |

| CGST + SGST vs IGST chosen by place of supply | Yes Auto from state code | No You decide each time | Partial Formula per sheet |

| Advance "receipt voucher" before the supply | Yes Built-in type | No Not handled | No Not handled |

| Print-ready PDF for email or WhatsApp | Yes One tap | Partial Export needed | No Looks like a spreadsheet |

Common mistakes to avoid

- Calling a quote an invoice. A proforma invoice is not a demand for payment and should never be entered in your sales register.

- Issuing a bill of supply when a tax invoice is required. If you are a regular registered dealer selling taxable goods, your buyer needs the GST split to claim ITC.

- Treating an invoice as proof of payment. An unpaid invoice proves what is owed, not what was paid — for reimbursement you need a receipt marked "Paid."

- Skipping or repeating invoice numbers. Numbers must be unique and sequential or your GSTR-1 filing breaks.

- Forgetting the revenue stamp on cash rent receipts. A ₹1 revenue stamp is required when cash rent on a single receipt exceeds ₹5,000 — see the rent receipt format for HRA.

- Mixing up CGST/SGST and IGST. Use CGST + SGST for same-state supply and IGST only for inter-state sales.

Sources & references

- CBIC GST Portal(opens in new tab) — tax invoice, bill of supply, and receipt voucher rules

- GST Council(opens in new tab) — registration thresholds and rate notifications

- Income Tax Department(opens in new tab) — record-keeping and HRA documentation

- India Code(opens in new tab) — CGST Act, 2017 (statutory text)

Need to send a payment request or confirm a payment? Create an invoice, bill, or receipt free → — no sign-up, instant PDF.