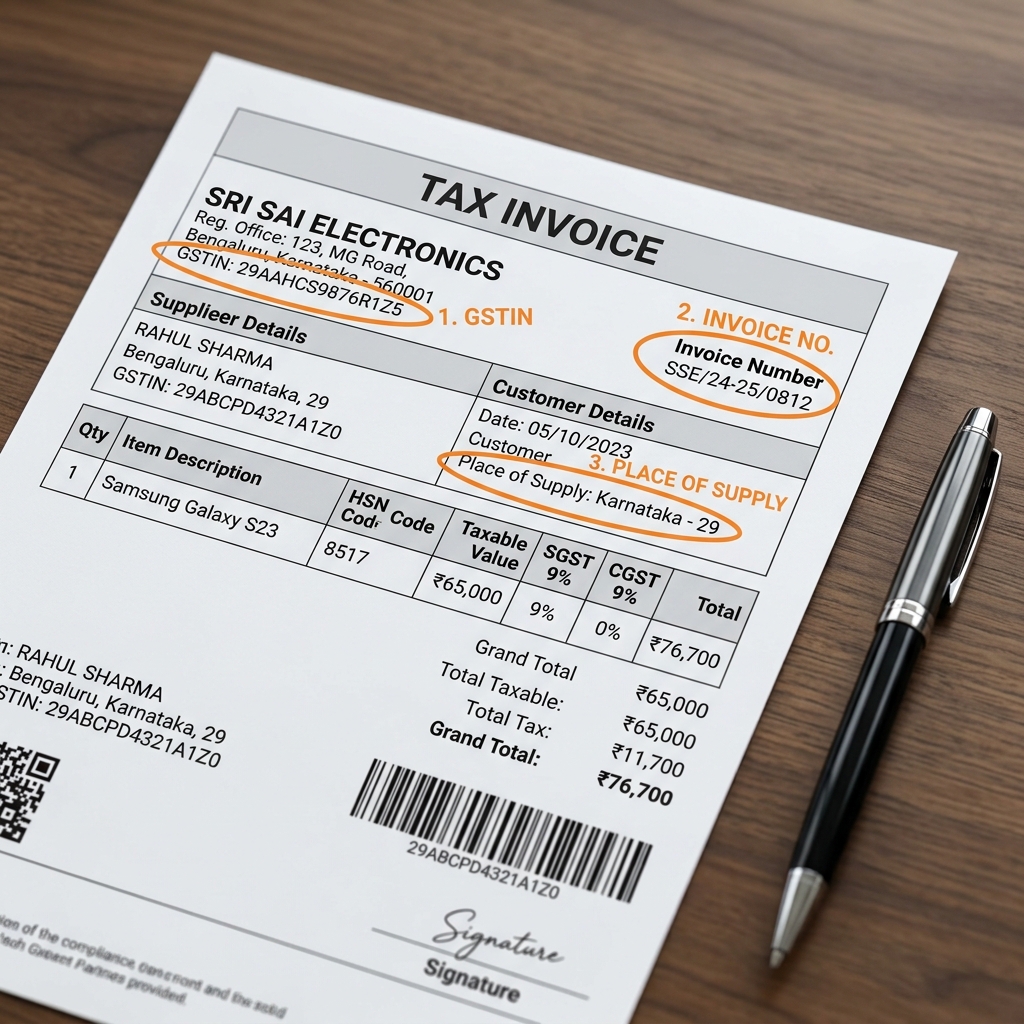

A GST bill — formally a tax invoice — must include the supplier's name, address and GSTIN, a unique sequential invoice number and date, the recipient's details, the HSN/SAC code, a description, quantity and value of what is supplied, the taxable value and tax breakup (CGST + SGST or IGST), the place of supply, and the supplier's signature. These fields are mandated by Rule 46 of the CGST Rules, 2017. Miss any of them and the invoice is non-compliant, and your buyer may lose their input tax credit.

Quick answer: the mandatory GST invoice fields

A valid GST tax invoice must carry:

- Supplier details — legal name, address, and 15-digit GSTIN

- Invoice number — unique, sequential, max 16 characters, and date of issue

- Recipient details — name, address, and GSTIN (if registered)

- HSN code (goods) or SAC code (services)

- Description, quantity, unit and value of goods/services

- Taxable value after any discount

- Tax rate and amount — split into CGST + SGST/UTGST, or IGST

- Place of supply (with state name and code) for inter-state sales

- Reverse charge indication, if applicable

- Signature or digital signature of the supplier/authorised person

Mandatory fields (and why each one matters)

Competitors list these fields. Here is what each one is actually for — and what goes wrong when it is missing.

| # | Field | Example | Why it matters |

|---|---|---|---|

| 1 | Supplier name & address | Reddy Hardware & Fabricators, 22 HITEC City Road, Madhapur, Hyderabad, Telangana 500081 | Identifies who is liable for the tax; establishes the location of supply |

| 2 | Supplier GSTIN | 36AAFCH6677S1Z5 | Proves registration; without it the document is not a valid tax invoice |

| 3 | Invoice number | INV-2026-00471 | Must be unique, sequential and ≤ 16 characters; the spine of your GSTR-1 |

| 4 | Invoice date | 01 Jun 2026 | Fixes the tax period and the time of supply |

| 5 | Recipient name & address | Deccan Infra Projects Pvt Ltd, Gachibowli, Hyderabad 500032 | Identifies the buyer; required for B2B input tax credit |

| 6 | Recipient GSTIN | 36AAACD4521P1ZK | Lets the buyer claim ITC; mandatory if the buyer is registered |

| 7 | HSN / SAC code | 7308 (steel structures) / 998719 (maintenance) | Classifies the supply; drives the correct tax rate and GSTR-1 summary |

| 8 | Description of goods/services | MS fabricated steel frame | Transparency and audit trail |

| 9 | Quantity & unit | 12 NOS | Basis for valuation and ITC matching |

| 10 | Taxable value | ₹1,80,000 | The value GST is charged on, after discount |

| 11 | Tax rate & amount | 18% → CGST ₹16,200 + SGST ₹16,200 | The legally required tax and its split |

| 12 | Place of supply | Telangana (36) | Decides whether CGST+SGST or IGST applies |

| 13 | Reverse charge | "Tax payable on reverse charge: No" | Tells the buyer who pays the tax |

| 14 | Signature | Authorised signatory sign / DSC | Validates the document under Rule 46 |

Tax invoice vs bill of supply. If you are not charging GST — because you are under the composition scheme or supplying exempt goods — you issue a bill of supply, not a tax invoice, and it must say so and omit the tax amount. A regular registered dealer making taxable supplies always issues a tax invoice. See invoice vs bill vs receipt for where each document fits.

Annotated sample GST invoice (filled example)

Here is a complete intra-state B2B tax invoice with realistic dummy data. Note how every Rule 46 field appears.

TAX INVOICE Reddy Hardware & Fabricators (Prop. Sneha Reddy) 22 HITEC City Road, Madhapur, Hyderabad, Telangana 500081 GSTIN: 36AAFCH6677S1Z5 · State: Telangana (36) Invoice No: INV-2026-00471 · Date: 01 Jun 2026 Reverse Charge: No

Bill to: Deccan Infra Projects Pvt Ltd, Gachibowli, Hyderabad, Telangana 500032 Recipient GSTIN: 36AAACD4521P1ZK · Place of Supply: Telangana (36)

| # | Description | HSN | Qty | Rate (₹) | Taxable (₹) |

|---|---|---|---|---|---|

| 1 | MS Fabricated Steel Frame | 7308 | 12 | 15,000 | 1,80,000 |

| 2 | Anti-corrosion Coating Service | 998719 | 1 | 20,000 | 20,000 |

| Total taxable value | 2,00,000 | ||||

| CGST @ 9% | 18,000 | ||||

| SGST @ 9% | 18,000 | ||||

| Invoice total | 2,36,000 |

Amount in words: Two Lakh Thirty-Six Thousand Rupees Only. For Reddy Hardware & Fabricators — Authorised Signatory (sign / DSC).

Because the supplier and buyer are both in Telangana, this is an intra-state supply, so the 18% tax splits into 9% CGST + 9% SGST. Had the buyer been in Karnataka, a single 18% IGST line would replace the CGST/SGST split and the place of supply would read "Karnataka (29)".

Legal & compliance: the GST invoice rules (FY 2025–26)

The mandatory contents of a tax invoice are governed by Rule 46 of the Central Goods and Services Tax Rules, 2017, read with Sections 31 and 34 of the CGST Act, 2017. The authoritative text is on the CBIC GST portal(opens in new tab) and India Code(opens in new tab).

Invoice numbering. The invoice number must be consecutive, unique for a financial year, and no longer than 16 characters — letters, numbers, "-" and "/" only. You may run separate series (e.g. one per branch), but each must be internally sequential. A fresh series can start each financial year.

HSN / SAC code requirement. As of FY 2025–26, the number of HSN digits depends on aggregate turnover in the preceding year:

| Aggregate turnover (preceding FY) | HSN/SAC digits required |

|---|---|

| Up to ₹5 crore | 4 digits |

| Above ₹5 crore | 6 digits |

For B2C supplies, businesses with turnover up to ₹5 crore are not required to quote HSN, although most do for clarity. Getting the code right also fixes your rate — see how to calculate GST on an invoice.

CGST + SGST vs IGST. The tax breakup is not optional. For an intra-state supply you must show CGST and SGST (or UTGST in union territories) as separate lines; for an inter-state supply you show a single IGST line. The deciding factor is the place of supply versus the supplier's location.

Signature. Rule 46 requires a signature or digital signature of the supplier or an authorised representative. Electronically transmitted invoices with a valid digital signature, and invoices generated under the e-invoicing (IRN + QR code) system, do not need a physical signature.

E-invoicing threshold. Under the e-invoicing mandate, businesses whose aggregate turnover exceeds ₹5 crore must generate an Invoice Reference Number (IRN) and QR code from the Invoice Registration Portal for B2B supplies. An invoice in this bracket that lacks a valid IRN is not treated as a valid tax invoice, and the buyer cannot claim input tax credit on it. Confirm the current threshold on cbic-gst.gov.in(opens in new tab), as it has been lowered in stages.

Number of copies. For goods, prepare three copies — Original for Recipient, Duplicate for Transporter, Triplicate for Supplier. For services, two copies — Original for Recipient and Duplicate for Supplier.

Time limit to issue. For goods, issue the invoice on or before removal/delivery; for services, within 30 days of supply (45 days for banks, NBFCs and insurers).

A note on fuel. Petrol, diesel, natural gas, ATF and crude oil are currently outside GST — they attract VAT and central excise instead. So a petrol-pump receipt will not show CGST/SGST. Do not "add GST" to a fuel bill to make it look like a tax invoice; that is a fabricated document. Keep fuel records as they are for reimbursement and accounting — our guide on whether you can make your own fuel bill explains the line between formatting a genuine receipt and faking one.

Legitimate record-keeping vs fraud. Issuing or reconstructing a GST invoice for a genuine sale you actually made is normal compliance. Creating an invoice for a sale that never happened, inflating values, or copying another firm's GSTIN is invoice fraud under the GST law and can trigger penalties and prosecution. A bill generator helps you format a real transaction correctly — it does not, and should not, manufacture fake supplies. If you are still deciding which document a given transaction even calls for, the invoice vs bill vs receipt breakdown and our GST bill generator walkthrough are good next reads.

Create a GST-compliant bill in 2 minutes

You do not need accounting software to issue one correct invoice. Using the bill & invoice generator:

- Choose the GST invoice template — it lays out every Rule 46 field for you.

- Enter your business details — legal name, address and GSTIN (saved for reuse).

- Add the buyer — name, address and GSTIN; set the place of supply.

- Add line items — description, HSN/SAC, quantity and rate; the tool computes the taxable value and the CGST + SGST or IGST automatically based on the states.

- Add your signature and download a clean, print-ready PDF — ready to email or send on WhatsApp.

The same flow feeds straight into your GSTR-1 preparation because the invoice numbers stay sequential and the HSN summary is already captured.

Online generator vs Word vs Excel/manual

| Rule 46 capability | Online generator | MS Word | Excel / manual |

|---|---|---|---|

| Splits 18% into CGST + SGST (or one IGST line) on its own | Yes Automatic | No You type each line | Partial Only if the formula is right |

| Picks intra- vs inter-state from the two states | Yes Decided for you | No Easy to get backwards | No Manual judgement |

| Validates the 15-digit GSTIN and its state code | Yes Checks format | No No check | No No check |

| Prompts for HSN/SAC at the digit count your turnover needs | Yes Built-in field | Partial Blank cell only | Partial Blank cell only |

| Keeps invoice numbers sequential and ≤ 16 characters | Yes Auto-increment | No Duplicates slip in | Partial Manual sort |

| Spells the invoice total in words | Yes Generated | No Type it yourself | No Type it yourself |

| Exports a clean, print-ready tax-invoice PDF | Yes One click | Partial Layout drifts | No Not really |

Common mistakes to avoid

- Skipping or repeating invoice numbers — this breaks your GSTR-1 trail and is the first thing an auditor notices.

- Showing IGST on an intra-state sale (or vice-versa) — the CGST/SGST-vs-IGST choice follows the place of supply, not habit.

- Omitting the HSN/SAC code when your turnover requires it — a missing or wrong code can hold up the buyer's ITC matching.

- Charging tax on exempt or nil-rated goods — if no GST applies, issue a bill of supply, not a tax invoice.

- Leaving out the signature on a printed invoice, or assuming a typed name counts as a signature.

- Printing an expired or copied GSTIN — verify it on the GST portal; an invalid GSTIN voids the customer's input tax credit and exposes you to penalty.

Sources & references

- CBIC GST Portal(opens in new tab) — CGST Rules (Rule 46), tax invoice format, e-invoicing and HSN notifications

- India Code(opens in new tab) — CGST Act, 2017 (Sections 31 & 34) and CGST Rules, 2017

- GST Council(opens in new tab) — rate and rule-change decisions

- Income Tax Department(opens in new tab) — PAN and cross-references for business records

Ready to issue a Rule 46-compliant invoice right now? Create a GST bill free → — no sign-up, automatic tax breakup, instant PDF.